On this article, I am going to introduce Monte Carlo simulations, clarify their relevance in buying and selling, and describe a selected choices buying and selling technique I’ve developed utilizing these simulations. I am going to additionally share backtested outcomes as an example the technique’s effectiveness.

1. What Are Monte Carlo Simulations?

Monte Carlo simulations are a computational approach used to mannequin the chance of various outcomes in a professionalcess that can’t simply be predicted as a result of presence of random variables. Named after the famed on line casino, these simulations are particularly helpful in finance as a result of they permit for the evaluation of uncertainty and danger.

The method includes working 1000’s and even tens of millions of simulations based mostly on historic value actions, the place every simulation initiatives a doable future consequence. The ensuing distribution offers merchants with possibilities of value ranges over a given time horizon.

2. How Are Monte Carlo Simulations Utilized in Trading?

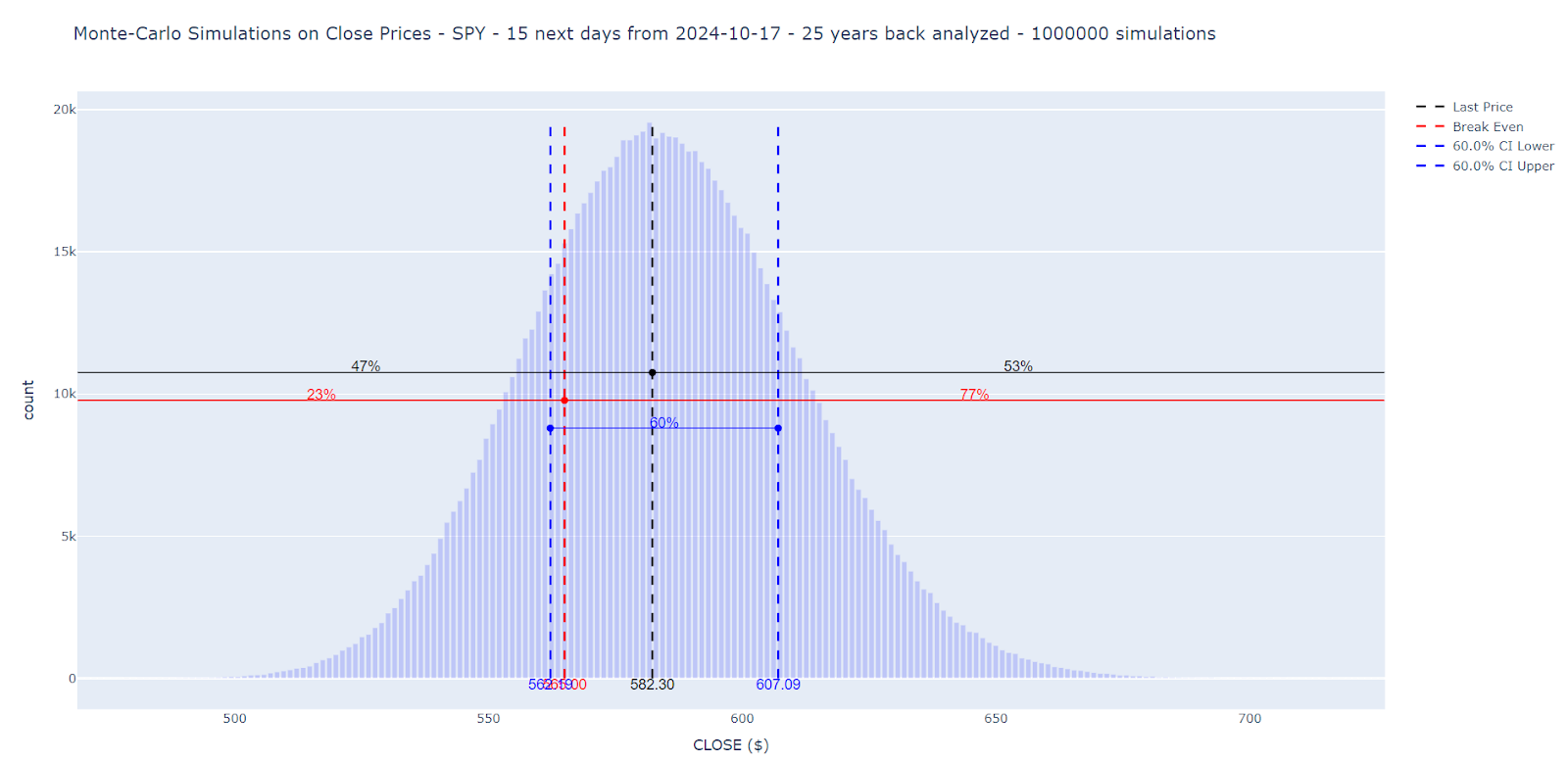

In buying and selling, Monte Carlo simulations assist to anticipate how a monetary instrument, similar to an ETF like SPY or QQQ, would possibly behave over a future interval. The method appears again over a number of years of historic value knowledge and runs quite a few simulations to venture future value distributions. The outputs sometimes present a chance distribution of future costs, highlighting key metrics similar to confidence intervals.Right here is an instance for SPY:

These simulations are invaluable for choices merchants as a result of they provide insights into the chance {that a} inventory or ETF will stay inside above/beneath value bounds over a selected time-frame. This info helps to craft structured choices methods, like Credit score Put Spreads, which revenue when an asset stays above a value threshold.

3. Instance for a Credit score Put Unfold

Right here for instance is the results of 10,000 simulations carried out on SPY for a prediction of the motion in 15 days by asking the algorithm to calculate what proportion of information is above the $565 threshold. For instance if we think about that this worth is a help or that this worth could be the break even of a Credit score Put Unfold technique that we’d have applied.

We see that there’s a chance of 77% that the ticker is above this threshold worth.

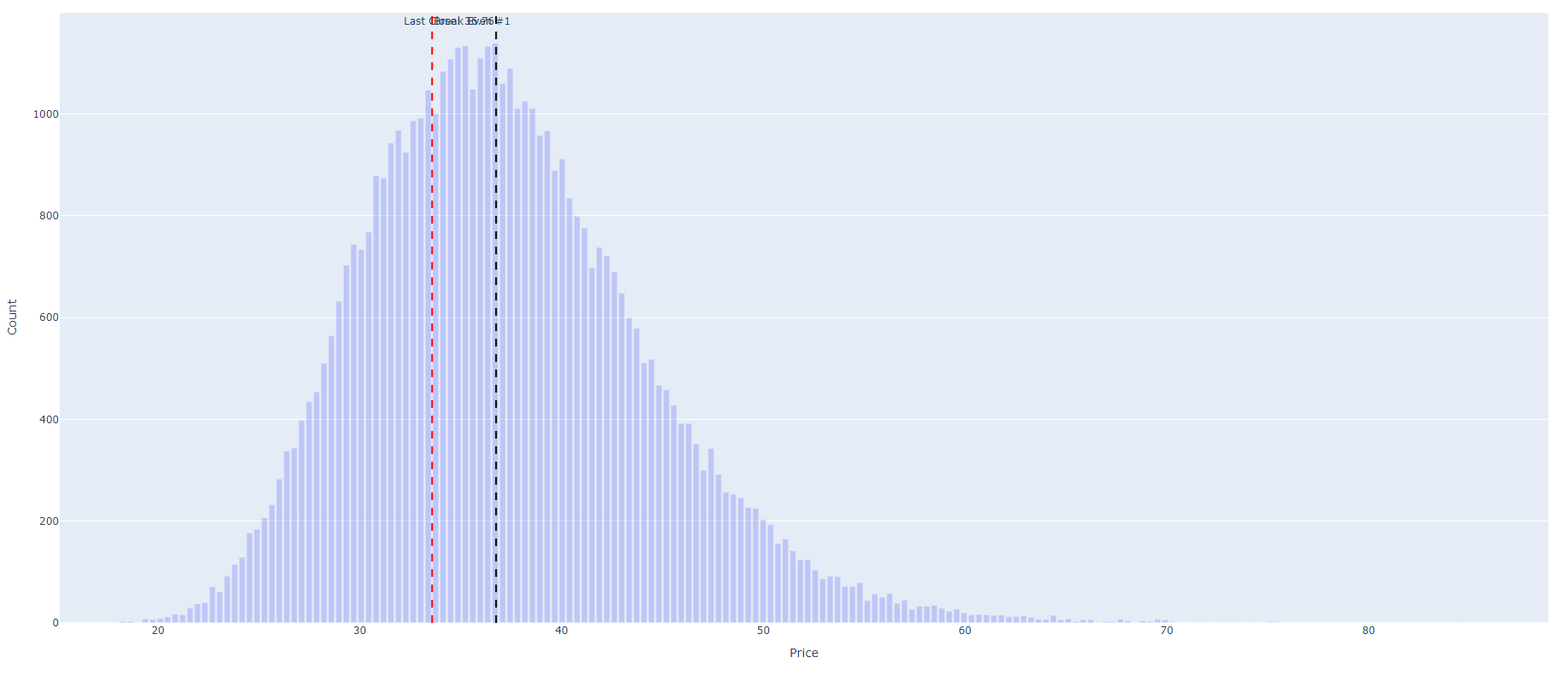

Recall that Monte Carlo simulations observe the previous habits of the ticker over a few years, day after day, deduce a statistical distribution and carry out random pictures oriented like this statistical distribution with a view to seize the pseudo-random nature of the market. It will likely be essential to see how these predictions have come true up to now.

Word that to account for the historic distribution of a ticker, we have to modify the Monte Carlo simulation method within the code. Moderately than assuming a traditional distribution for value actions, I mannequin value modifications based mostly on the precise historic distribution of returns. This system, typically referred to as bootstrapping, samples historic returns instantly as an alternative of producing artificial returns based mostly on a hard and fast regular distribution.

That is then the sort of plot we get :

4. The Technique: Utilizing Monte Carlo Simulations for Choices Trading

Utilizing the break evens of an Iron Condor as threshold values isn’t attention-grabbing as a result of the simulations confirmed that credit obtained on the Name half weren’t ample.

So let’s give attention to the Put half by way of Credit score Put Spreads. For a given ETF (we are going to pass over shares due to the earnings), there are lots of expiration dates and lots of strikes, every with their very own value. Which ETF to decide on, which strikes to purchase and promote and which expiration dates?

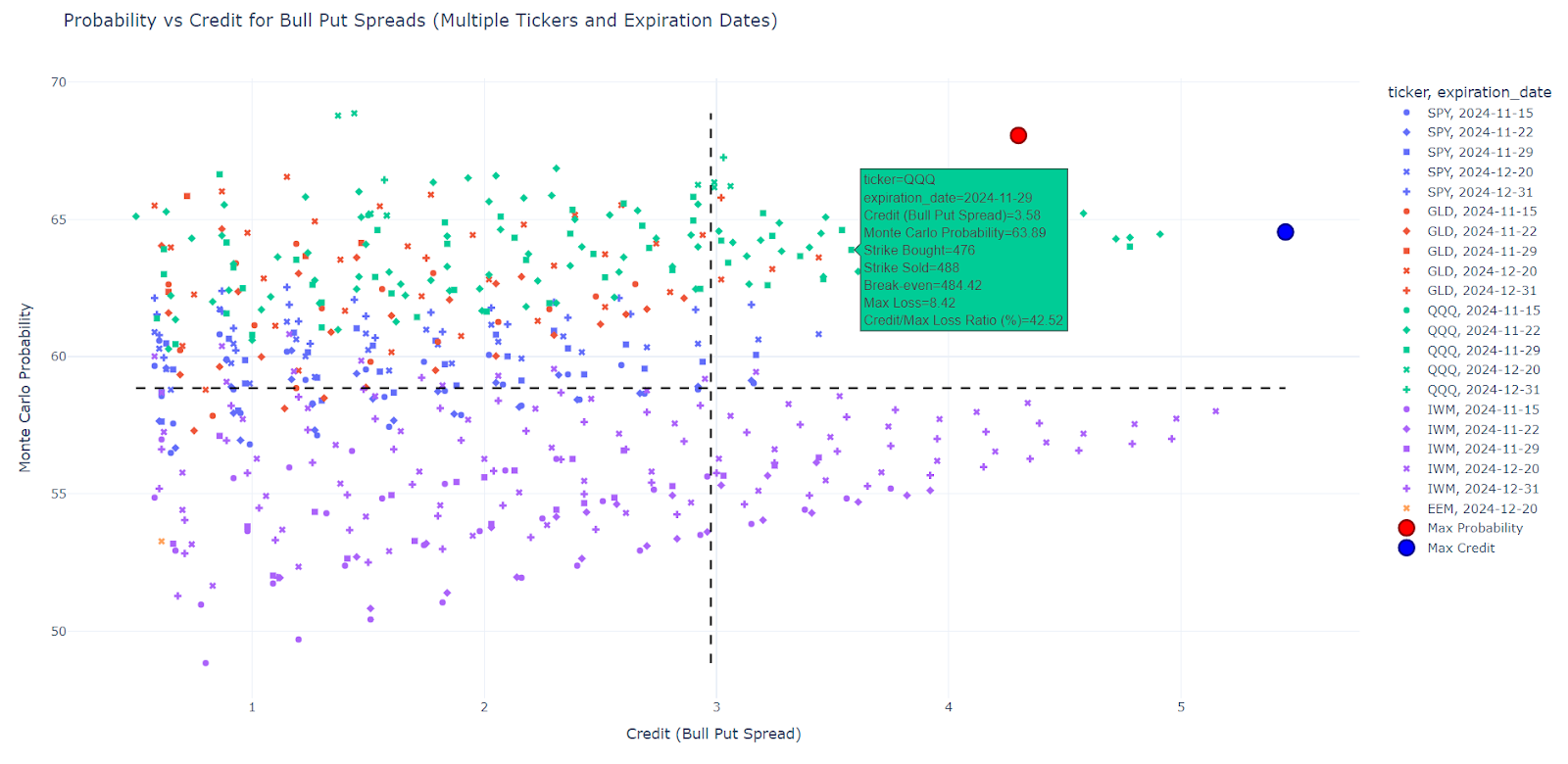

For this, this system I wrote scans an important ETFs, [‘SPY’,’GLD’,’QQQ’,’IWM’,’EEM’], all their expiration dates between two numbers of days [min_days = 30 max_days = 120] and all strikes beneath the OTM strike that may kind a Credit score Put Unfold. Some extent is thus given by, for instance, [SPY, 2024-11-15, put bought=$577, put sold=$582].

For every level, the code then performs 10,000 Monte Carlo simulations, trying again 20 years and calculating the chance that the SPY shut might be larger than the break even in 29 days (=variety of days remaining between now and the expiration date). Then, this system shows all of the factors within the type of a graph with, on the abscissa, the perceived credit score and on the ordinate, the Monte Carlo chance. Credit score > $0.50 and acquire/loss ratio above 40% are solely chosen.

The graph is split into 4 quadrants, the considered one of most curiosity to us being the northeast quadrant (most credit score and most chance). This system then detects the 2 factors which, on this quadrant, have the best chance or the best credit score.

Right here is an instance of show:

4. Backtesting Outcomes

To validate this technique, we carried out backtests utilizing historic knowledge for the previous 15 years. The concept was to simulate what would have occurred if this technique had been utilized up to now with the break even comparable to the chance computed within the chosen level.

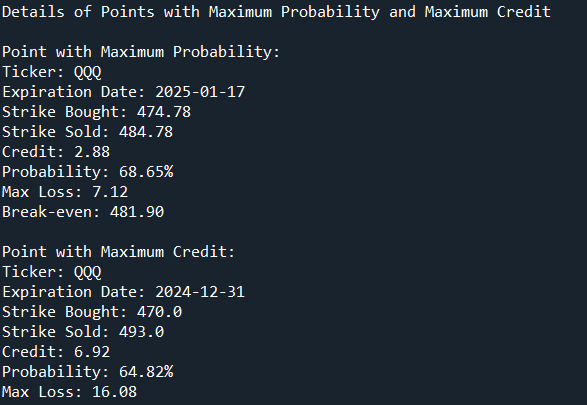

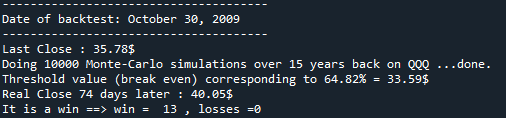

To make use of the instance right here above with the utmost credit score,the backtest would reply this query: for the ticker QQQ on the expiration date of 2024-12-31 (comparable to 74 days from now, the date of writing this text), the Monte Carlo simulations inform me that the Shut of QQQ has a chance of 64.82% of being larger than the technique’s break even. If I had utilized this technique 15 years up to now from now, day after day with the Break Even at the moment comparable to this quantile, would the actual worth of QQQ have certainly been larger than this Break Even? And if that’s the case, what number of occasions has it labored between 15 years in the past and now, day after day?

To be extra particular, through the backtest the algorithm shows the outcomes of the step-by-step backtests very clearly:

Instance of a screenshot through the backtest:

and the plot of the histogram to show the consistency of the brink worth:

This systematic method, with exact danger administration, offers merchants with a robust software to make knowledgeable choices about structuring choices trades. It is value noting that the efficiency of every technique can range relying on market circumstances, so constant backtesting is essential to retaining the technique worthwhile in evolving markets.

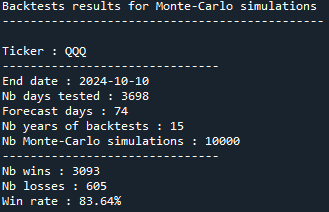

The ultimate results of the backtest, for that technique, is:

Which means that backtests give higher outcomes (83.64% win charge) than the chances introduced by Monte Carlo simulations (64.82%) and the commerce may very well be opened.

Conclusion

Monte Carlo simulations provide a scientific and data-driven strategy to venture future value ranges within the typically unpredictable world of buying and selling. By making use of these simulations, we will develop methods that goal to seize worth by precisely predicting value actions inside particular time horizons. The backtests present that utilizing this methodology, particularly for long-term choices methods like Iron Condors, can considerably enhance the probability of success.

This method enhances different choices methods and offers a strong framework for structuring trades with a excessive chance of revenue, whereas rigorously managing danger.